Don’t slight historical wisdom

Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

In an era of instant gratification, it should not be a surprise that the market has been trending ahead of itself. The competitive nature of this country has developed technology, produced goods, created wealth and shaped our world prominence. Perhaps some of this competitive nature has seeped into our desire to be first to predict the future. Perhaps it’s about crafting media sensationalism to prop viewership. Perhaps it’s about a craze that rewards originality even in the face of historical wisdom. Whatever the reason, it feels like we have been pressing the issues. In the midst of this chaos, clients yearn for a clear picture of our economic path while figureheads demand precision timing and exact answers on how events will play out. I’ve been in this game for over thirty years and for however much that collective wisdom counts, the only thing I can say with certainty is that there is none. However, economic cycles often follow similar patterns and historic analysis can unfold a reasonable likelihood serving to assist investors with appropriate fixed income investing.

Consider this commentary as a trailer to this week’s release of the Fixed Income Quarterly which is dedicated to correlating our current economic cycle with historic economic patterns. More importantly, it reveals how this elevated interest rate environment has extended a very unique fixed income opportunity to not only serve as a guard for one’s wealth but aid as an impactful income tool.

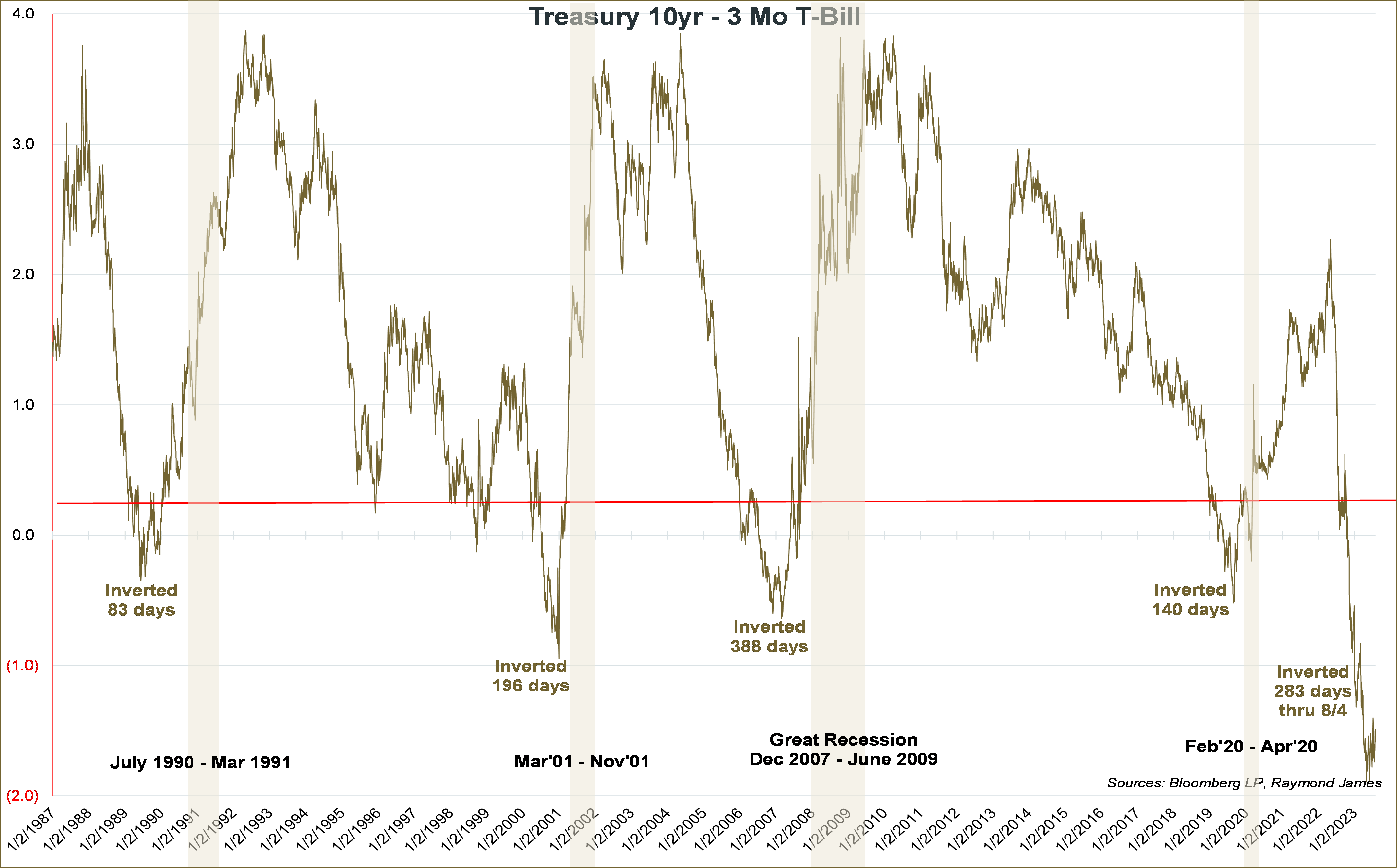

One takeaway is that inverted curves precede recessions. You will hear arguments that this isn’t always true but that viewpoint isolates mini-time ranges rather than viewing wide ranges of time as depicted on this graph. It also seems reasonable to note that the longest inversion period resulted in the longest recession (December 2007 to June 2009). Lastly, the ensuing recessions start on average, 4-5 months after the curve normalizes and becomes upward-sloping.

The past does not necessarily predict the future, but it may be sensible to put more weight on how economic cycles have played out over more than 30 years of time before adhering to the latest sensational claim. If history is our guide, the current economic cycle is in the midst of accumulating a very long inverted period (286 days). A subsequent recession is likely months away as the yield curve has yet to “normalize”. This is in sync with the Fed’s focus on curtailing inflation and their continued associated tightening policy. It also permits time for the economy to absorb the effects of continued interest rate hikes. This series of events is propping up interest rates and providing investors with a window of opportunity to lock in healthy income. When the cycle completes itself, interest rates are likely to fall. Please look for the upcoming Fixed Income Quarterly which will uncover related historic patterns and help to analyze appropriate fixed income strategies for your investment portfolio.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.